10 Mistakes to Avoid When Looking for Quotes on Term Life Insurance

One of the most important financial decisions you will ever make is shopping for term-life insurance. This is a simple product with competitive prices for a limited period, but getting a term life policy quote comparison wrong can be surprisingly easy. Making a wrong move might result in you paying more, getting the wrong policy, or even having your application denied.

Whether you are shopping for term-life insurance policy quotes for the first time or looking at your existing policy, these common mistakes will help you get the proper term life policy quotes without unnecessary hassle or expense.

Mistake 1: Only Considering the Cost

Although receiving the lowest monthly payments is important, buying the cheapest term life policy without considering the reliability of the insurance company may be a costly mistake in the future. While the cost may be low, it is not important if the insurance company has a complicated process or does not have the means to pay out your policy.

Mistake 2: Underestimating the Amount of Coverage Required

Don't merely estimate the amount of coverage you require. Rather, double your annual salary by 10 to 15 percent as a general rule, then add any outstanding loans (such as your mortgage) and future costs (such as your child's college tuition). Don't undervalue the significance of these elements, or your family may receive a price for a term life insurance policy that looks excellent on paper but isn't sufficient to pay their costs.

Mistake 3: Putting Off Applying for Too Long

The two most crucial elements in deciding the price of your life insurance policy are your age and health. Your rates may increase the longer you wait to apply, making them potentially unaffordable in the future. Therefore, now is the ideal time to apply if you're in good health so that you can obtain reasonably priced term-life insurance for the future.

Mistake 4: Believing That Group Life Insurance Is Sufficient

Having group life insurance offered by the company can be a wonderful perk. However, this is not sufficient. The coverage offered by group life insurance is usually in multiples of the salary. It is usually 1 to 2 times the salary. Additionally, when you leave the company, you also lose the life insurance. The quote offered in term life insurance can be tailored and taken with you when you leave.

Mistake 5: Not Comparing Multiple Quotes

It can be tempting to go with the first life insurance provider you hear about, but the premium rates can vary significantly between companies. It is a good idea to get at least 3 to 5 quotes for a term life policy before you make a decision. The significance of health factors varies between companies, and a high rate at one company can be a preferred rate at another.

Mistake 6: Lying on Your Application

You may be tempted to lie on your application if you are trying to hide your weight problem, your smoking habit, or your medical condition. Well, let me tell you something. Insurers will have access to your medical records, your prescription records, and your driving record. Therefore, if they find that there are discrepancies between your application and your medical records, your application will not only be declined, but your policy will also be rescinded, and your death benefits will not be paid out if you die.

Mistake 7: Ignoring the Conversion Option

Term life policies usually have a conversion option that will enable you to convert your term life policy to a permanent policy without undergoing medical tests. Of course, this is a great opportunity if you are diagnosed with a serious medical condition in the future. While shopping for a term life policy, you should determine whether your policy has a conversion option, when to convert your policy, and what type of policy to convert to.

Mistake 8: Choosing a Term that is Too Short

It is important to note that the term that is chosen should match your financial commitments. For example, a 10-year term may not be sufficient to cover your kids when they are in college if you still have young kids at home. Ten years, fifteen years, twenty years, and thirty years are the most common terms that are used. The term that is right for you is the term that matches your retirement goals, your kids' independence goals, or your mortgage goals.

Mistake 9: Overlooking Permanent Insurance Alternatives

While term insurance is ideal for temporary coverage, some consumers overlook the fact that permanent insurance may be a better solution for meeting their long-term objectives. In fact, there are some relatively affordable permanent life insurance products, such as whole life or guaranteed universal life, that may be a better solution depending on your objectives. While term insurance is perfect for temporary coverage, permanent insurance may be an alternative solution depending on your objectives.

Mistake 10: Delaying the Decision

Analysis paralysis. Quotes. Research on companies. And then… nothing. Time is passing. Health can change. Interest rates can rise. But the best time to buy life insurance was yesterday. The second-best time to buy life insurance is today.

Getting It Right

Purchasing life insurance doesn't have to be difficult. By avoiding these common mistakes, you'll be well on your way to getting the right life insurance policy to meet your needs at a price you can afford. The end goal in getting a term-life insurance quote isn't just to get a quote. It's about getting peace of mind, knowing that no matter what life throws at you, you'll be able to take care of those you love.

Categorias

Leia mais

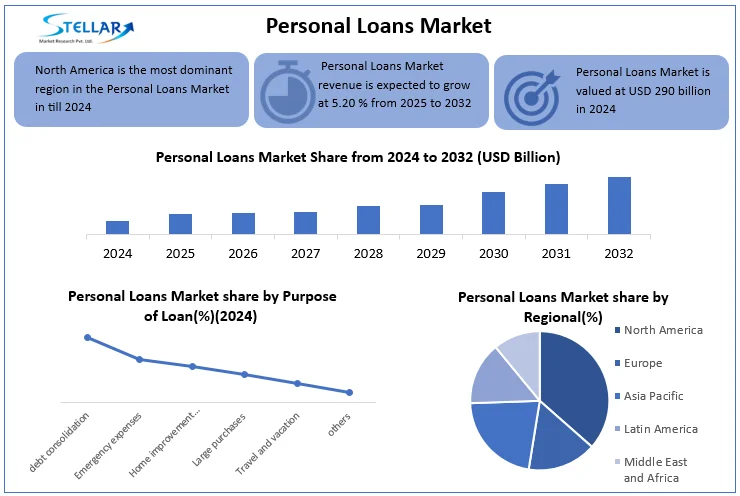

Personal Loans Market was estimated at USD 290 billion in 2024 and is expected to reach USD 435.03 billion in 2032. CAGR is expected to be around 5.20% during the forecast period (2025-2032). Personal Loans Market Overview Stellar Market Research is a Business Consultancy Firm that has published a detailed analysis of the “Personal Loans Market”. The report includes key...

When it comes to dependable and comfortable group travel, EasyWay Limo stands out as a trusted name for Shuttle Bus Transportation Englewood. Whether you are planning corporate travel, airport transfers, family gatherings, or special events, having a reliable transportation partner makes all the difference. EasyWay Limo specializes in providing seamless travel experiences through its...

Choosing the right mobile app development company helps organizations create reliable tools that support customer engagement and business efficiency. Mobile App Development focuses on designing applications that combine usability with technical strength for companies operating in the UAE. What Sets Professional Development Apart Structured workflows and planning Custom design instead of...

Streetwear has transformed the global fashion industry, blending casual clothing with bold cultural expression. Among the brands that helped shape this movement, Stüssy stands as one of the most influential names. From its humble beginnings in California to its worldwide popularity today, Stussy has remained a powerful symbol of creativity, individuality, and urban style. One of the...

L'Univers Krosmoz De l'étreinte primordiale entre deux forces, naquit un cosmos aux dimensions plurielles. Cet œuf-univers, nommé Krosmoz, abrite les galaxies où prennent vie Dofus et Wakfu. Il est le reflet d'une identité créative unique, mais aussi le socle d'ambitions stratégiques grandissantes. Comme l'entité qui lui donna naissance,...